2012 DSE 企业会计与财务概论-BAFS 真题 答案 详解

2012-05-04 dse dse 企业会计与财务概论-BAFS

| 序号 | 文件列表 | 说明 | ||

|---|---|---|---|---|

| 1 | 2012-企业会计与财务概论-BAFS-answer-zh.pdf | 19 页 | 2.78MB | 答案(中文) |

| 2 | 2012-企业会计与财务概论-BAFS-answer-eng.pdf | 20 页 | 2.75MB | 答案(英文) |

| 3 | 2012-企业会计与财务概论-BAFS-paper1-zh.pdf | 12 页 | 2.52MB | 真题 Paper 1(中文) |

| 4 | 2012-企业会计与财务概论-BAFS-paper1-eng.pdf | 10 页 | 882.13KB | 真题 Paper 1(英文) |

| 5 | 2012-企业会计与财务概论-BAFS-paper2a-zh.pdf | 8 页 | 1.71MB | 真题 Paper 2a(中文) |

| 6 | 2012-企业会计与财务概论-BAFS-paper2b-zh.pdf | 5 页 | 1.00MB | 真题 Paper 2b(中文) |

| 7 | 2012-企业会计与财务概论-BAFS-paper2a-eng.pdf | 7 页 | 920.73KB | 真题 Paper 2a(英文) |

| 8 | 2012-企业会计与财务概论-BAFS-paper2b-eng.pdf | 3 页 | 280.30KB | 真题 Paper 2b(英文) |

答案(中文)

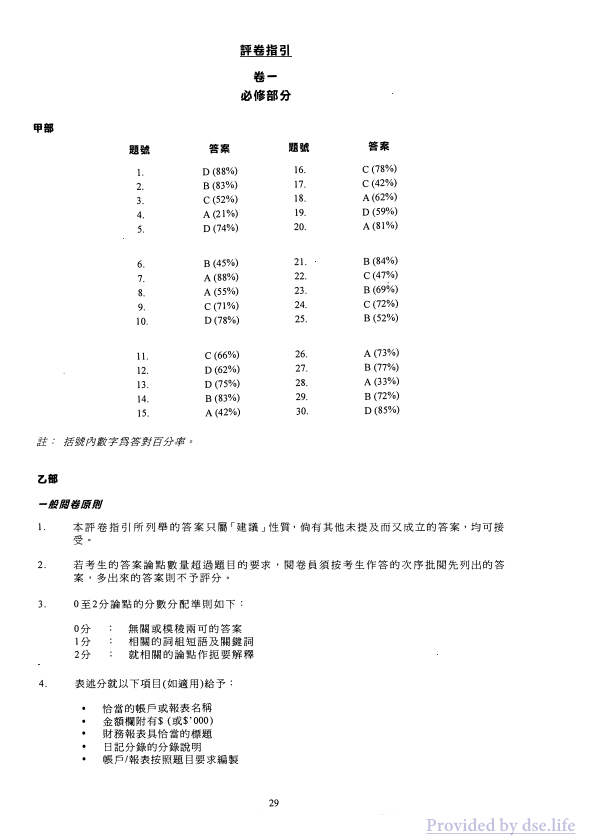

評卷指引

卷一

必修部分

甲部

| 题号 | 答案 | 题号 | 答案 |

|---|---|---|---|

| 1 | D(88%) | 16 | C(78%) |

| 2 | B(83%) | 17 | C(42%) |

| 3 | C(52%) | 18 | A(62%) |

| 4 | A(21%) | 19 | D(59%) |

| 5 | D(74%) | 20 | A(81%) |

| 6 | B(45%) | 21 | B(84%) |

| 7 | A(88%) | 22 | C(47%) |

| 8 | A(55%) | 23 | B(69%) |

| 9 | C(71%) | 24 | C(72%) |

| 10 | D(78%) | 25 | B(52%) |

| 11 | C(66%) | 26 | A(73%) |

| 12 | D(62%) | 27 | B(77%) |

| 13 | D(75%) | 28 | A(33%) |

| 14 | B(83%) | 29 | B(72%) |

| 15 | A(42%) | 30 | D(85%) |

註:括號內數字為答對百分率。

乙部

一般閱卷原則

-

本評卷指引所列舉的答案只屬「建議」性質,倘有其未提及而又成立的答案,均可接受。

-

若考生的答案論點數量超過題目的要求,閱卷員須按考生作答的次序批閱先列出的答案,多出來的答案則不予評分。

-

0至2分論點的分數分配則如下:

0分 : 無關或模棱兩可的答案

1分 : 相關的詞組短語及關鍵詞

2分 : 就相關的論點作扼要解釋

-

表述分就以下項目(如適用)給予:

-

恰當的帳戶或報表名稱

- 金額欄附有$ (或$'000)

- 財務報表具恰當的標題

- 日記分錄的分錄說明

- 帐户/报表按照题目要求编制

29

Provided by dse.life

答案(英文)

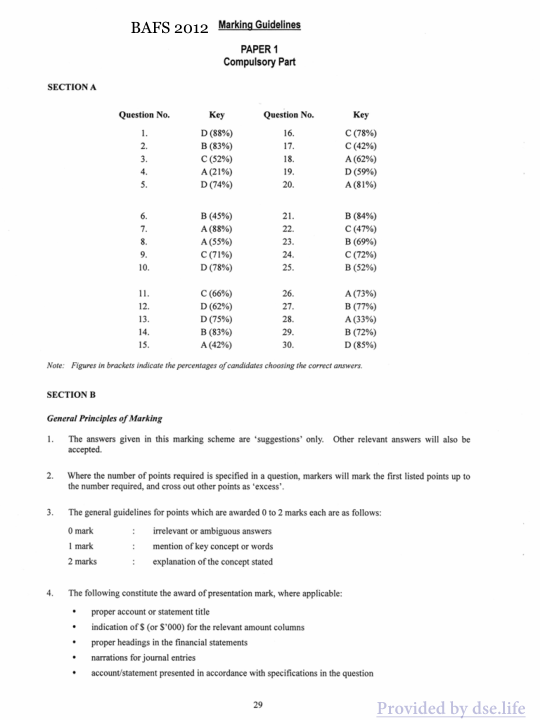

BAFS 2012 Marking Guidelines

PAPER 1 Compulsory Part

SECTION A

Question No. Key Question No. Key

1. D (88%) 16. C (78%)

2. B (83%) 17. C (42%)

3. C (52%) 18. A (62%)

4. A (21%) 19. D (59%)

5. D (74%) 20. A (81%)

6. B (45%) 21. B (84%)

7. A (88%) 22. C (47%)

8. A (55%) 23. B (69%)

9. C (71%) 24. C (72%)

10. D (78%) 25. B (52%)

11. C (66%) 26. A (73%)

12. D (62%) 27. B (77%)

13. D (75%) 28. A (33%)

14. B (83%) 29. B (72%)

15. A (42%) 30. D (85%)

Note: Figures in brackets indicate the percentages of candidates choosing the correct answers.

SECTION B

General Principles of Marking

1. The answers given in this marking scheme are ‘suggestions’ only. Other relevant answers will also be accepted.

2. Where the number of points required is specified in a question, markers will mark the first listed points up to the number required, and cross out other points as ‘excess’.

3. The general guidelines for points which are awarded 0 to 2 marks each are as follows:

- 0 mark : irrelevant or ambiguous answers

- 1 mark : mention of key concept or words

- 2 marks : explanation of the concept stated

4. The following constitute the award of presentation mark, where applicable:

- proper account or statement title

- indication of $ (or $'000) for the relevant amount columns

- proper headings in the financial statements

- narrations for journal entries

- account/statement presented in accordance with specifications in the question

29 Provided by dse.life

真题 Paper 1(中文)

2012-DSE 企業、會計與財務概論 卷一甲

香港考試及評核局 2012年香港中學文憑考試

企業、會計與財務概論 試卷一

本試卷必須用中文作答 一小時三十分鐘完卷(上午八時三十分至上午十時)

考生须知 (一) 本卷分甲、乙兩部。 (二) 甲部為多項選擇題,見於本試卷中;乙部的短答題另見於試題答题簿B之內。 (三) 甲部的答案須填畫在多項選擇題的答题紙上,而乙部的答案則須寫在試題答题簿B所预留的空位内。考试完毕,甲部之答题纸與乙部之试题答题薄B须分别缴交。

甲部的考生须知(多项选择题) (一) 細讀答题纸上的指示。宣布開考後,考生须首先於適當位置貼上電腦條碼及填上各项所需资料。宣布停筆後,考生不會獲得額外時間貼上電腦條碼。 (二) 試場主任宣布開卷後,考生须检查试题有否缺漏,最后一题之后应有「甲部完」字樣。 (三) 各题估分相等。 (四) 本试卷全部试题均须回答。为便於修正答案,考生宜用HB铅笔画把答案填畫在答题纸上。錯误答案可用潔淨膠擦將筆痕徹底擦去。考生须清楚填畫答案,否则會因答案未能被辨認而失分。 (五) 每题只可填畫一個答案,若填畫多個答案,則該题不给分。 (六) 答案錯誤,不另扣分。

考试結束前不可将试卷带離試場

2012-DSE-BAFS 1A-1

4

Provided by dse.life

真题 Paper 1(英文)

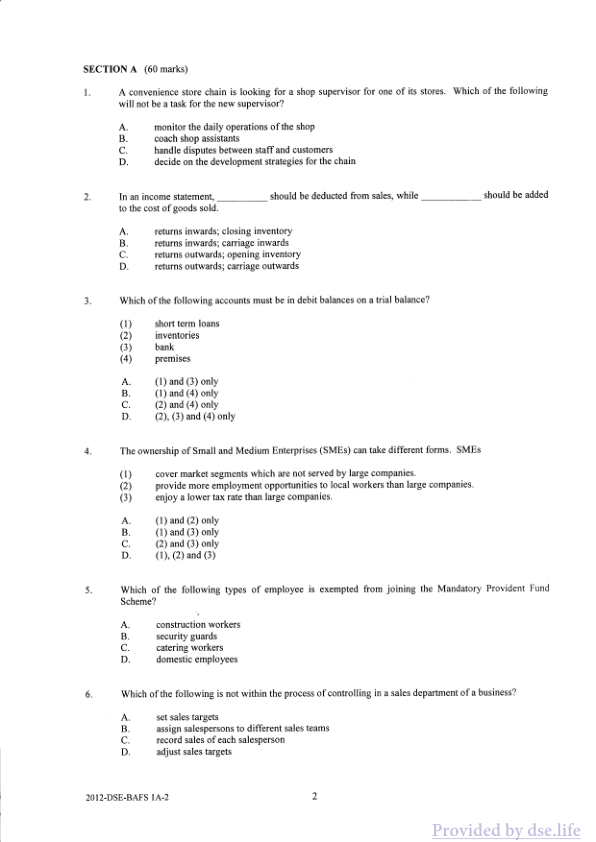

SECTION A (60 marks)

1. A convenience store chain is looking for a shop supervisor for one of its stores. Which of the following will not be a task for the new supervisor? A. monitor the daily operations of the shop B. coach shop assistants C. handle disputes between staff and customers D. decide on the development strategies for the chain

2. In an income statement, should be deducted from sales, while should be added to the cost of goods sold. A. returns inwards; closing inventory B. returns inwards; carriage inwards C. returns outwards; opening inventory D. returns outwards; carriage outwards

3. Which of the following accounts must be in debit balances on a trial balance? (1) short term loans (2) inventories (3) bank (4) premises A. (1) and (3) only B. (1) and (4) only C. (2) and (4) only D. (2), (3) and (4) only

4. The ownership of Small and Medium Enterprises (SMEs) can take different forms. SMEs (1) cover market segments which are not served by large companies. (2) provide more employment opportunities to local workers than large companies. (3) enjoy a lower tax rate than large companies. A. (1) and (2) only B. (1) and (3) only C. (2) and (3) only D. (1), (2) and (3)

5. Which of the following types of employee is exempted from joining the Mandatory Provident Fund Scheme? A. construction workers B. security guards C. catering workers D. domestic employees

6. Which of the following is not within the process of controlling in a sales department of a business? A. set sales targets B. assign salespersons to different sales teams C. record sales of each salesperson D. adjust sales targets

2012-DSE-BAFS 1A-2 2

Provided by dse.life

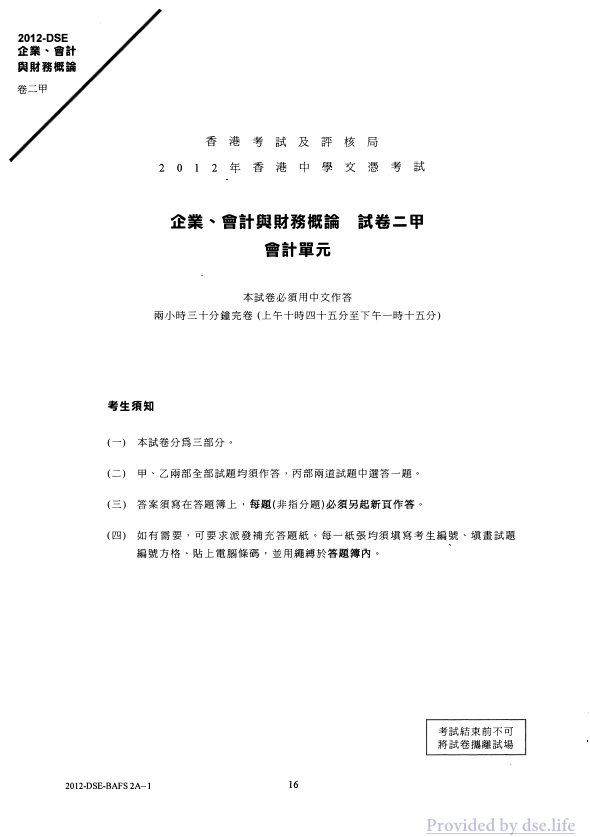

真题 Paper 2a(中文)

2012-DSE 企業、會計與財務概論 卷二甲

香港考試及評核局 2012年香港中學文憑考試

企業、會計與財務概論 試卷二甲 會計單元

本試卷必須用中文作答 兩小時三十分鐘完卷(上午十時四十五分至下午一時十五分)

考生须知 (一) 本試卷分為三部分。 (二) 甲、乙兩部全部試題均須作答,丙部兩道試題中選答一題。 (三) 答案須寫在答题簿上,每题(非指分题)必须另起新页作答。 (四) 如有需要,可要求派發補充答题纸。每一张均须填写考生编号、填涂试题编号、贴上电脑条码,並用绳带於答题簿内。

考试结束前不可将试卷带离考场

2012-DSE-BAFS 2A-1 16

Provided by dse.life

真题 Paper 2b(中文)

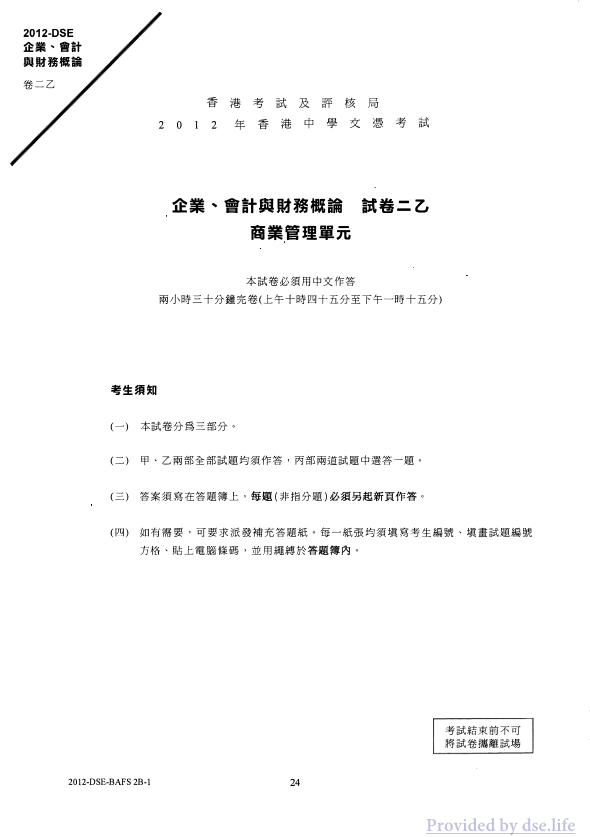

2012-DSE 企業、會計與財務概論 卷二乙

香港考試及評核局 2012年香港中學文憑考試

企業、會計與財務概論 試卷二乙 商業管理單元

本試卷必須用中文作答 兩小時三十分鐘完卷(上午十時四十五分至下午十一時十五分)

考生須知 (一) 本試卷分爲三部分。 (二) 甲、乙兩部全部試題均須作答,丙部兩道試題中選答一題。 (三) 答案須寫在答题簿上,每题(非指分题)必须另起新页作答。 (四) 如有需要,可要求派發補充答题纸。每一张均须填写考生编号、填盖试题编號方格、贴上電腦條碼,並用繩綁於答题簿内。

考试結束前不可将试卷攜離試場

2012-DSE-BAFS 2B-1 24

Provided by dse.life

真题 Paper 2a(英文)

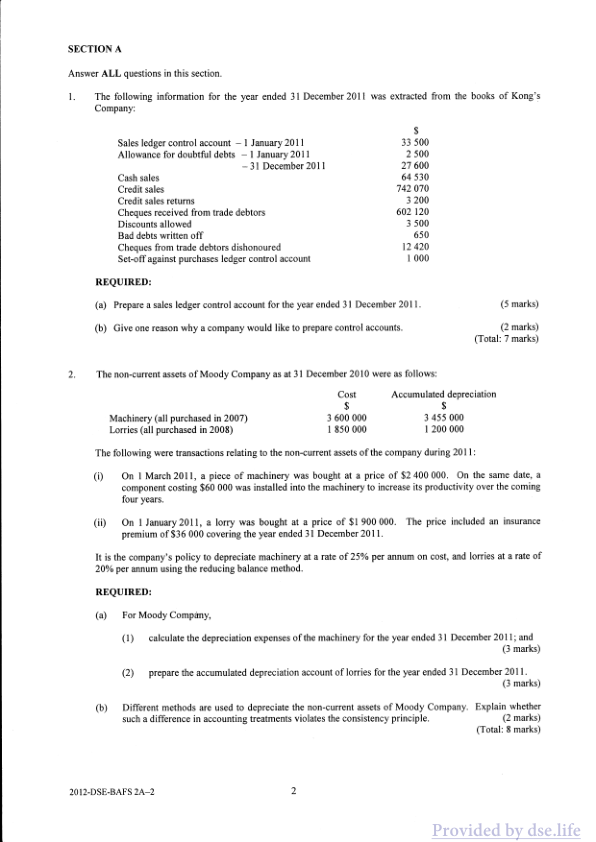

SECTION A

Answer ALL questions in this section.

- The following information for the year ended 31 December 2011 was extracted from the books of Kong's Company:

Sales ledger control account - 1 January 2011 $33 500

Allowance for doubtful debts - 1 January 2011 $2 500

- 31 December 2011 $27 600

Cash sales $64 530

Credit sales $742 070

Credit sales returns $3 200

Cheques received from trade debtors $602 120

Discounts allowed $3 500

Bad debts written off $650

Cheques from trade debtors dishonoured $12 420

Set-off against purchases ledger control account $1 000

REQUIRED:

(a) Prepare a sales ledger control account for the year ended 31 December 2011. (5 marks)

(b) Give one reason why a company would like to prepare control accounts. (2 marks)

(Total: 7 marks)

- The non-current assets of Moody Company as at 31 December 2010 were as follows:

Machinery (all purchased in 2007) Cost Accumulated depreciation

$3 600 000 $3 455 000

Lorries (all purchased in 2008) $1 850 000 $1 200 000

The following were transactions relating to the non-current assets of the company during 2011:

(i) On 1 March 2011, a piece of machinery was bought at a price of $2 400 000. On the same date, a component costing $60 000 was installed into the machinery to increase its productivity over the coming four years.

(ii) On 1 January 2011, a lorry was bought at a price of $1 900 000. The price included an insurance premium of $36 000 covering the year ended 31 December 2011.

It is the company's policy to depreciate machinery at a rate of 25% per annum on cost, and lorries at a rate of 20% per annum using the reducing balance method.

REQUIRED:

(a) For Moody Company,

(1) calculate the depreciation expenses of the machinery for the year ended 31 December 2011; and (3 marks)

(2) prepare the accumulated depreciation account of lorries for the year ended 31 December 2011. (3 marks)

(b) Different methods are used to depreciate the non-current assets of Moody Company. Explain whether such a difference in accounting treatments violates the consistency principle. (2 marks)

(Total: 8 marks)

2012-DSE-BAFS 2A-2

真题 Paper 2b(英文)

SECTION A

Answer ALL questions in this section.

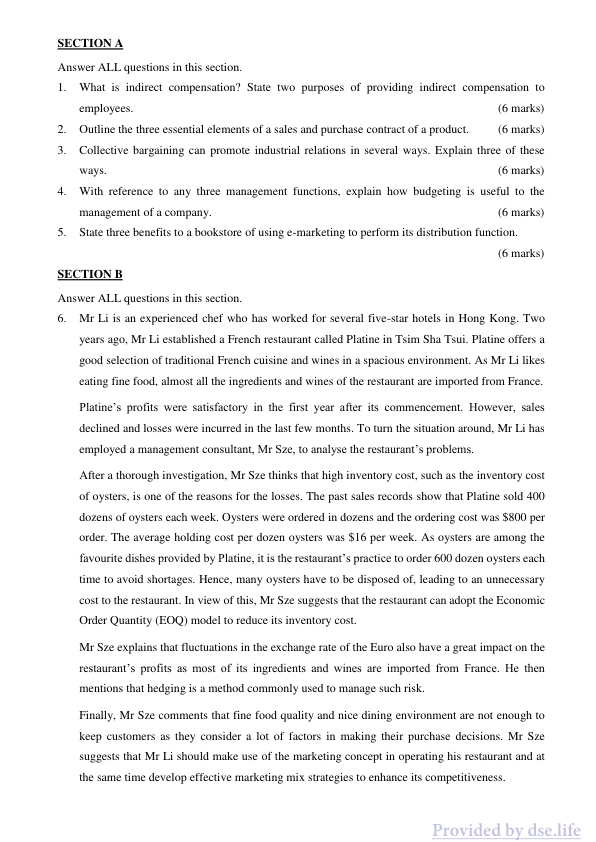

1. What is indirect compensation? State two purposes of providing indirect compensation to employees. (6 marks)

2. Outline the three essential elements of a sales and purchase contract of a product. (6 marks)

3. Collective bargaining can promote industrial relations in several ways. Explain three of these ways. (6 marks)

4. With reference to any three management functions, explain how budgeting is useful to the management of a company. (6 marks)

5. State three benefits to a bookstore of using e-marketing to perform its distribution function. (6 marks)

SECTION B

Answer ALL questions in this section.

6. Mr Li is an experienced chef who has worked for several five-star hotels in Hong Kong. Two years ago, Mr Li established a French restaurant called Platine in Tsim Sha Tsui. Platine offers a good selection of traditional French cuisine and wines in a spacious environment. As Mr Li likes eating fine food, almost all the ingredients and wines of the restaurant are imported from France. Platine’s profits were satisfactory in the first year after its commencement. However, sales declined and losses were incurred in the last few months. To turn the situation around, Mr Li has employed a management consultant, Mr Sze, to analyse the restaurant’s problems.

After a thorough investigation, Mr Sze thinks that high inventory cost, such as the inventory cost of oysters, is one of the reasons for the losses. The past sales records show that Platine sold 400 dozens of oysters each week. Oysters were ordered in dozens and the ordering cost was $800 per order. The average holding cost per dozen oysters was $16 per week. As oysters are among the favourite dishes provided by Platine, it is the restaurant’s practice to order 600 dozen oysters each time to avoid shortages. Hence, many oysters have to be disposed of, leading to an unnecessary cost to the restaurant. In view of this, Mr Sze suggests that the restaurant can adopt the Economic Order Quantity (EOQ) model to reduce its inventory cost.

Mr Sze explains that fluctuations in the exchange rate of the Euro also have a great impact on the restaurant’s profits as most of its ingredients and wines are imported from France. He then mentions that hedging is a method commonly used to manage such risk.

Finally, Mr Sze comments that fine food quality and nice dining environment are not enough to keep customers as they consider a lot of factors in making their purchase decisions. Mr Sze suggests that Mr Li should make use of the marketing concept in operating his restaurant and at the same time develop effective marketing mix strategies to enhance its competitiveness.

Provided by dse.life