2014 DSE 企业会计与财务概论-BAFS 真题 答案 详解

2014-05-07 dse dse 企业会计与财务概论-BAFS

| 序号 | 文件列表 | 说明 | ||

|---|---|---|---|---|

| 1 | 2014-企业会计与财务概论-BAFS-answer-eng.pdf | 18 页 | 3.13MB | 答案(英文) |

| 2 | 2014-企业会计与财务概论-BAFS-paper1-zh.pdf | 10 页 | 1.52MB | 真题 Paper 1(中文) |

| 3 | 2014-企业会计与财务概论-BAFS-paper1-eng.pdf | 10 页 | 2.22MB | 真题 Paper 1(英文) |

| 4 | 2014-企业会计与财务概论-BAFS-paper2a-zh.pdf | 7 页 | 597.90KB | 真题 Paper 2a(中文) |

| 5 | 2014-企业会计与财务概论-BAFS-paper2b-zh.pdf | 5 页 | 995.22KB | 真题 Paper 2b(中文) |

| 6 | 2014-企业会计与财务概论-BAFS-paper2a-eng.pdf | 8 页 | 386.33KB | 真题 Paper 2a(英文) |

| 7 | 2014-企业会计与财务概论-BAFS-paper2b-eng.pdf | 5 页 | 1.05MB | 真题 Paper 2b(英文) |

答案(英文)

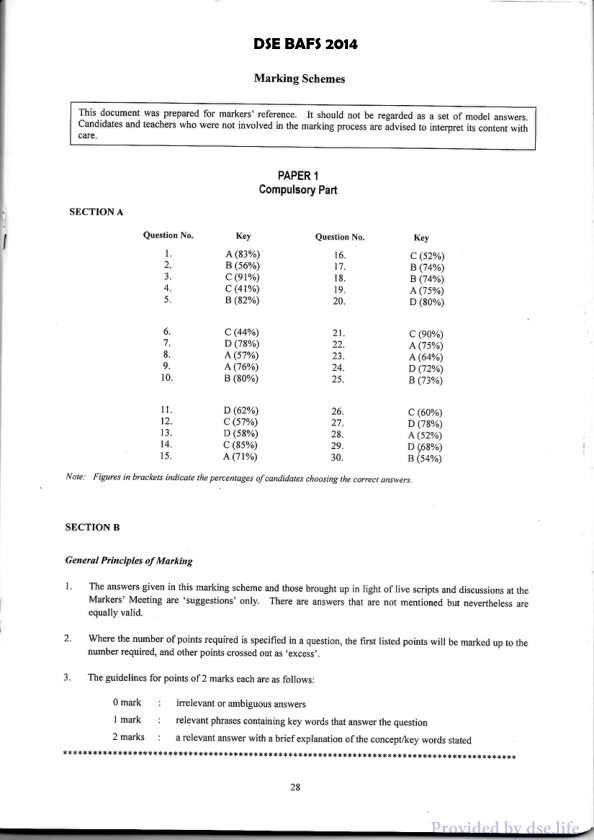

DSE BAFS 2014

Marking Schemes

This document was prepared for markers’ reference. It should not be regarded as a set of model answers. Candidates and teachers who were not involved in the marking process are advised to interpret its content with care.

PAPER 1

Compulsory Part

SECTION A

| Question No. | Key | Question No. | Key |

|---|---|---|---|

| 1 | A | 16 | C |

| 2 | B | 17 | B |

| 3 | C | 18 | B |

| 4 | C | 19 | A |

| 5 | B | 20 | D |

| 6 | C | 21 | C |

| 7 | D | 22 | A |

| 8 | A | 23 | A |

| 9 | A | 24 | D |

| 10 | B | 25 | B |

| 11 | D | 26 | C |

| 12 | C | 27 | D |

| 13 | D | 28 | A |

| 14 | C | 29 | D |

| 15 | A | 30 | B |

Note: Figures in brackets indicate the percentages of candidates choosing the correct answers.

SECTION B

General Principles of Marking

- The answers given in this marking scheme and those brought up in light of live scripts and discussions at the Markers’ Meeting are ‘suggestions’ only. There are answers that are not mentioned but nevertheless are equally valid.

- Where the number of points required is specified in a question, the first listed points will be marked up to the number required, and other points crossed out as ‘excess’.

- The guidelines for points of 2 marks each are as follows:

- 0 mark : irrelevant or ambiguous answers

- 1 mark : relevant phrases containing key words that answer the question

- 2 marks : a relevant answer with a brief explanation of the concept/key words stated

真题 Paper 1(中文)

2014-DSE 企業、會計與財務概論 卷一

香港考試及評核局 2014年香港中學文憑考試

企業、會計與財務概論 試卷一

本試卷必須用中文作答 一小時十五分鐘完卷(上午八時三十分至上午九時四十五分)

考生须知 (一) 本試卷分甲、乙兩部:甲部為多項選擇題,乙部為短題目。 (二) 甲部為必答题。乙部分為兩部分:第一部分全部試題均須作答,第二部分兩道試題中選答一題。 (三) 甲部的答案須填在多項選擇題答題紙上,乙部的答案須寫在答題簿上。每題(非指分題)必須另起新頁作答。 (四) 考試完畢,甲部的答題紙與乙部的答題簿須分别繳交。

甲部的考生须知(多項選擇題) (一) 細讀答題紙上的指示。宣布開考後,考生須首先於適當位置貼上電腦條碼及填上各項所需資料。宣布停筆後,考生不會獲得額外時間貼上電腦條碼。 (二) 試場主任宣布開卷後,考生須檢查試題有否缺漏,最後一題之後應有「甲部完」字樣。 (三) 各題估分相等。 (四) 全部試題均須作答。為便於修正答案,考生宜用HB鉛筆把答案填在答題紙上。錯誤答案可用濕淨膠擦將筆痕徹底擦去。考生須清楚填畫答案,否則會因答案未能被辨認而失分。 (五) 每題只可填畫一個答案,若填畫多個答案,則該題不給分。 (六) 答案錯誤,不另扣分。

考試結束前不可將試卷攜離試場

2014-DSE-BAFS 1-1

4

真题 Paper 1(英文)

2014-DSE BAFS PAPER 1

HONG KONG EXAMINATIONS AND ASSESSMENT AUTHORITY

HONG KONG DIPLOMA OF SECONDARY EDUCATION EXAMINATION 2014

BUSINESS, ACCOUNTING AND FINANCIAL STUDIES PAPER 1

8:30 am – 9:45 am (1 hour 15 minutes)

This paper must be answered in English

GENERAL INSTRUCTIONS

(1) There are TWO sections, A and B, in this Paper. Section A consists of multiple-choice questions and Section B contains short questions.

(2) Answer ALL questions in Section A. There are two parts in Section B: Answer ALL questions in Part 1 and ONE of the two questions in Part 2.

(3) Answers to Section A should be marked on the Multiple-choice Answer Sheet while answers to Section B should be written in the Answer Book. In the Answer Book, start EACH question (not part of a question) on a NEW page.

(4) The Answer Sheet for Section A and the Answer Book for Section B must be handed in separately at the end of the examination.

INSTRUCTIONS FOR SECTION A (MULTIPLE-CHOICE QUESTIONS)

(1) Read carefully the instructions on the Answer Sheet. After the announcement of the start of the examination, you should first stick a barcode label and insert the information required in the spaces provided. No extra time will be given for sticking on the barcode label after the ‘Time is up’ announcement.

(2) When told to open this book, you should check that all the questions are there. Look for the words ‘END OF SECTION A’ after the last question.

(3) All questions carry equal marks.

(4) ANSWER ALL QUESTIONS. You are advised to use an HB pencil to mark all the answers on the answer sheet, so that wrong marks can be completely erased with a clean rubber. You must mark the answers clearly; otherwise you will lose marks if the answers cannot be captured.

(5) You should mark only ONE answer for each question. If you mark more than one answer, you will receive NO MARKS for that question.

(6) No marks will be deducted for wrong answers.

Not to be taken away before the end of the examination session

2014-DSE-BAFS 1-1

4

Provided by dse.life

真题 Paper 2a(中文)

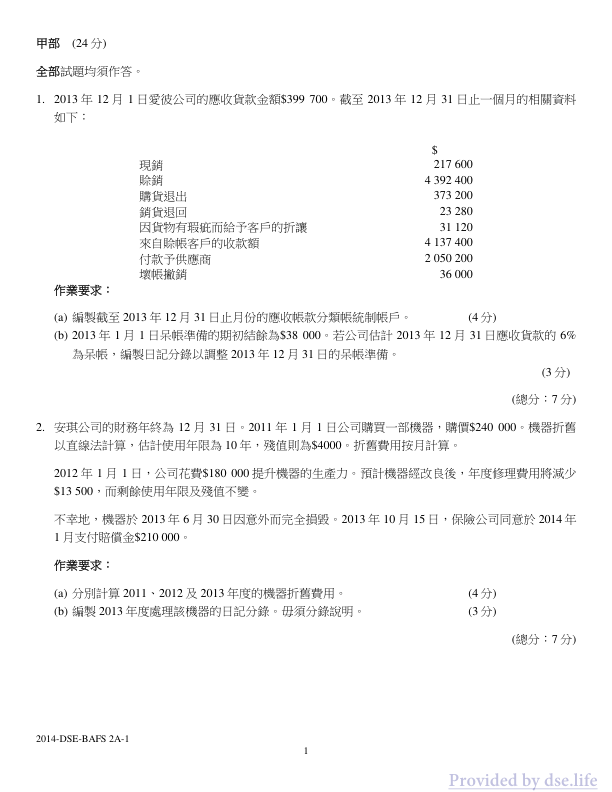

甲部 (24分)

全部試題均須作答。

- 2013年12月1日愛彼公司的應收賬款金額$399 700。截至2013年12月31日止一個月的相關資料如下:

現銷 $217 600

脫銷 4 392 400

購貨退出 373 200

銷貨退回 23 280

因貨物有瑕疵而給予客户的折讓 31 120

來自脫帳客户的收款額 4 137 400

付款予供應商 2 050 200

環帐撤銷 36 000

作業要求: (a) 编製截至2013年12月31日止月份的應收賬款分類賬統制賬戶。 (4分) (b) 2013年1月1日呆帐備的期初結餘為$38 000。若公司估計2013年12月31日應收賬款的6% 為呆帐,编製日記分錄以調整2013年12月31日的呆帐備。 (3分) (總分:7分)

- 安琪公司的財務年終為12月31日。2011年1月1日公司購買一部機器,購價$240 000。機器折舊以直線法計算,估計使用年限為10年,殘值則為$4000。折舊費用按月計算。 2012年1月1日,公司花費$180 000提升機器的生產力。預計機器經改良後,年度修理費用將減少$13 500,而剩餘使用年限及殘值不變。 不幸地,機器於2013年6月30日因意外而完全損毁。2013年10月15日,保險公司同意於2014年1月支付賠償金$210 000。

作業要求: (a) 分別計算2011、2012及2013年度的機器折舊費用。 (4分) (b) 编製2013年度處理該機器的日記分錄。毋須分錄說明。 (3分) (總分:7分)

2014-DSE-BAFS 2A-1 1

Provided by dse.life

真题 Paper 2b(中文)

2014-DSE 企業、會計 與財務概論 卷二乙

香港考試及評核局 2014年香港中學文憑考試

企業、會計與財務概論 試卷二乙 商業管理單元

本試卷必須用中文作答 兩小時十五分鐘完卷(上午十時三十分至下午十二時四十五分)

考生須知: (一) 本試卷分爲三部分。 (二) 甲、乙兩部全部試題均須作答,丙部兩道試題中選答一題。 (三) 答案須寫在答题簿上,每题(非指分题)必须另起新页作答。

考試結束前不可 將試卷攜離試場

2014-DSE-BAFS 2B-1 22

Provided by dse.life

真题 Paper 2a(英文)

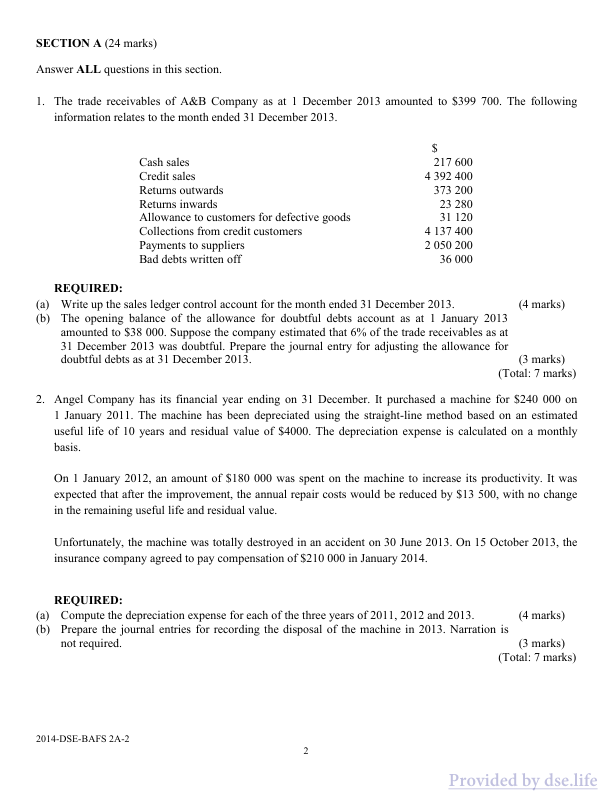

SECTION A (24 marks) Answer ALL questions in this section. 1. The trade receivables of A&B Company as at 1 December 2013 amounted to $399 700. The following information relates to the month ended 31 December 2013.

| $ | |

|---|---|

| Cash sales | |

| Credit sales | |

| Returns outwards | |

| Returns inwards | |

| Allowance to customers for defective goods | |

| Collections from credit customers | |

| Payments to suppliers | |

| Bad debts written off |

REQUIRED: (a) Write up the sales ledger control account for the month ended 31 December 2013. (4 marks) (b) The opening balance of the allowance for doubtful debts account as at 1 January 2013 amounted to $38 000. Suppose the company estimated that 6% of the trade receivables as at 31 December 2013 was doubtful. Prepare the journal entry for adjusting the allowance for doubtful debts as at 31 December 2013. (Total: 7 marks)

- Angel Company has its financial year ending on 31 December. It purchased a machine for $240 000 on 1 January 2011. The machine has been depreciated using the straight-line method based on an estimated useful life of 10 years and residual value of $4000. The depreciation expense is calculated on a monthly basis.

On 1 January 2012, an amount of $180 000 was spent on the machine to increase its productivity. It was expected that after the improvement, the annual repair costs would be reduced by $13 500, with no change in the remaining useful life and residual value.

Unfortunately, the machine was totally destroyed in an accident on 30 June 2013. On 15 October 2013, the insurance company agreed to pay compensation of $210 000 in January 2014.

REQUIRED: (a) Compute the depreciation expense for each of the three years of 2011, 2012 and 2013. (4 marks) (b) Prepare the journal entries for recording the disposal of the machine in 2013. Narration is not required. (3 marks) (Total: 7 marks)

2014-DSE-BAFS 2A-2 2 Provided by dse.life

真题 Paper 2b(英文)

2014-DSE BAFS PAPER 2B HONG KONG EXAMINATIONS AND ASSESSMENT AUTHORITY HONG KONG DIPLOMA OF SECONDARY EDUCATION EXAMINATION 2014 BUSINESS, ACCOUNTING AND FINANCIAL STUDIES PAPER 2B Business Management Module 10:30 am – 12:45 pm (2 hours 15 minutes) This paper must be answered in English INSTRUCTIONS (1) There are three sections in this paper. (2) All questions in Sections A and B are compulsory. You are required to answer one of the two questions in Section C. (3) Write your answers in the answer book. Start each question (not part of a question) on a new page. Not to be taken away before the end of the examination session 2014-DSE-BAFS 2B-1 23 Provided by dee life