2016 DSE 企业会计与财务概论-BAFS 真题 答案 详解

2016-05-08 dse dse 企业会计与财务概论-BAFS

| 序号 | 文件列表 | 说明 | ||

|---|---|---|---|---|

| 1 | 2016-企业会计与财务概论-BAFS-answer-zh.pdf | 17 页 | 7.84MB | 答案(中文) |

| 2 | 2016-企业会计与财务概论-BAFS-answer-eng.pdf | 17 页 | 8.68MB | 答案(英文) |

| 3 | 2016-企业会计与财务概论-BAFS-paper1-zh.pdf | 9 页 | 478.50KB | 真题 Paper 1(中文) |

| 4 | 2016-企业会计与财务概论-BAFS-paper1-eng.pdf | 9 页 | 398.67KB | 真题 Paper 1(英文) |

| 5 | 2016-企业会计与财务概论-BAFS-paper2a-zh.pdf | 9 页 | 537.23KB | 真题 Paper 2a(中文) |

| 6 | 2016-企业会计与财务概论-BAFS-paper2b-zh.pdf | 5 页 | 2.52MB | 真题 Paper 2b(中文) |

| 7 | 2016-企业会计与财务概论-BAFS-paper2a-eng.pdf | 8 页 | 407.39KB | 真题 Paper 2a(英文) |

| 8 | 2016-企业会计与财务概论-BAFS-paper2b-eng.pdf | 4 页 | 1.31MB | 真题 Paper 2b(英文) |

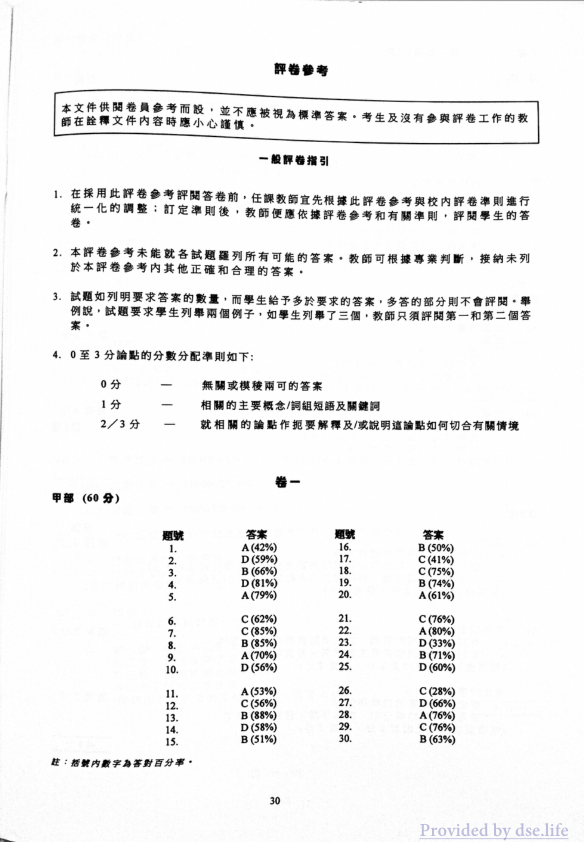

答案(中文)

評卷參考

本文件供閱卷員參考而設,並不應被視為標準答案。考生及沒有參與評卷工作的教師在針對文件內容時應小心謹慎。

一般評卷指引

-

在採用此評卷參考評閱答卷前,任課教師宜先根據此評卷參考與校內評卷則進行統一化的調整;訂定準則後,教師便應依據評卷參考和有關準則,評閱學生的答卷。

-

本評卷參考未能就各試題羅列所有可能的答案。教師可根據專業判斷,接納未列於本評卷參考內其他正確和合理的答案。

-

試題如列明要求答案的数量,而學生給予多於要求的答案,多答的部分則不會評閱。舉例說,試題要求學生列出兩個例子,如學生列了三個,教師只須評閱第一和第二個答案。

-

0至3分論點的分數分配準則如下:

0分 無關或模糊兩可的答案

1分 相關的主要概念/詞組短語及關鍵詞

2/3分 就相關的論點作扼要解釋及/或說明這論點如何切合有關情境

卷一

甲部(60分)

题號 答案 题号 答案

1. A(42%) 16. B(50%)

2. D(59%) 17. C(41%)

3. B(66%) 18. C(75%)

4. D(81%) 19. B(74%)

5. A(79%) 20. A(61%)

6. C(62%) 21. C(76%)

7. C(85%) 22. A(80%)

8. B(85%) 23. D(33%)

9. A(70%) 24. B(71%)

10. D(56%) 25. D(60%)

11. A(53%) 26. C(28%)

12. C(56%) 27. D(66%)

13. B(88%) 28. A(76%)

14. D(58%) 29. C(76%)

15. B(51%) 30. B(63%)

注:括號内数字为答对百分率·

30

Provided by dse.life

答案(英文)

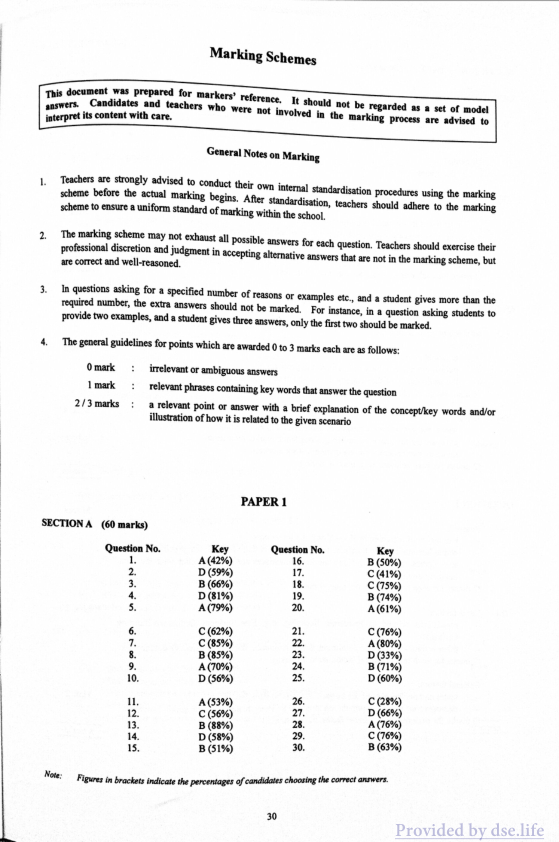

Marking Schemes

This document was prepared for markers' reference. It should not be regarded as a set of model answers. Candidates and teachers who were not involved in the marking process are advised to interpret its content with care.

General Notes on Marking

- Teachers are strongly advised to conduct their own internal standardisation procedures using the marking scheme before the actual marking begins. After standardisation, teachers should adhere to the marking scheme to ensure a uniform standard of marking within the school.

- The marking scheme may not exhaust all possible answers for each question. Teachers should exercise their professional discretion and judgment in accepting alternative answers that are not in the marking scheme, but are correct and well-reasoned.

- In questions asking for a specified number of reasons or examples etc., and a student gives more than the required number, the extra answers should not be marked. For instance, in a question asking students to provide two examples, and a student gives three answers, only the first two should be marked.

- The general guidelines for points which are awarded 0 to 3 marks each are as follows:

- 0 mark: irrelevant or ambiguous answers

- 1 mark: relevant phrases containing key words that answer the question

- 2/3 marks: a relevant point or answer with a brief explanation of the concept/key words and/or illustration of how it is related to the given scenario

PAPER 1

SECTION A (60 marks)

| Question No. | Key | Question No. | Key |

|---|---|---|---|

| 1 | A (42%) | 16 | B (50%) |

| 2 | D (59%) | 17 | C (41%) |

| 3 | B (66%) | 18 | C (75%) |

| 4 | D (81%) | 19 | B (74%) |

| 5 | A (79%) | 20 | A (61%) |

| 6 | C (62%) | 21 | C (76%) |

| 7 | C (85%) | 22 | A (80%) |

| 8 | B (85%) | 23 | D (33%) |

| 9 | A (70%) | 24 | B (71%) |

| 10 | D (56%) | 25 | D (60%) |

| 11 | A (53%) | 26 | C (28%) |

| 12 | C (56%) | 27 | D (66%) |

| 13 | B (88%) | 28 | A (76%) |

| 14 | D (58%) | 29 | C (76%) |

| 15 | B (51%) | 30 | B (63%) |

Note: Figures in brackets indicate the percentages of candidates choosing the correct answers.

Provided by dse.life

真题 Paper 1(中文)

甲部(60分)

本部分共30题,全部试题均需作答。考生应选取各题最通切的答案。

- 下列哪项是位于香港的跨国公司的特徵? (1) 它們也會在香港以外地方營運。 (2) 它們都在香港的證券交易所上市。 (3) 它們的僱員人數多於100。

A. 只有(1) B. 只有(1)及(2) C. 只有(2)及(3) D. (1)、(2)及(3)

- 相對於高架式架構,下列哪項是扁平式架構的特點? (1) 控制幅度較闊 (2) 管理層層數較少 (3) 決策過程较短

A. 只有(1)及(2) B. 只有(1)及(3) C. 只有(2)及(3) D. (1)、(2)及(3)

-

在一家按地域劃分不同部門的公司, A. 部門辦公室設立於在部門所管轄的區域。 B. 部門經理負責他所管轄區域的企業營運。 C. 部門銷售點只會出售部門所管轄區域生產的貨物。 D. 部門只在所管轄區域內聘請員工。

-

安娜剛在65歲退休,她收到一筆可觀的公積金。她計劃將公積金作投資以獲得一些回報,但卻不欲承擔高風險。下列哪項投資工具最不合她? A. 定期存款 B. 储蓄存款 C. 通脈掛鉤債券 D. 股票

-

心美是瑪莉商號的客户,信贷记录良好。截至2015年12月31日止年度,瑪莉除購货物$8000予心美。心美於2016年1月借清该项货欠。根据_(1)__,玛莉愿记该交易为___(2)___年度的销售。

A. 應計概念 2015 B. 應計概念 2016 C. 继续经营假设 2015 D. 继续经营假设 2016

2016-DSE-BAFS 1-2 2

Provided by dse.life

真题 Paper 1(英文)

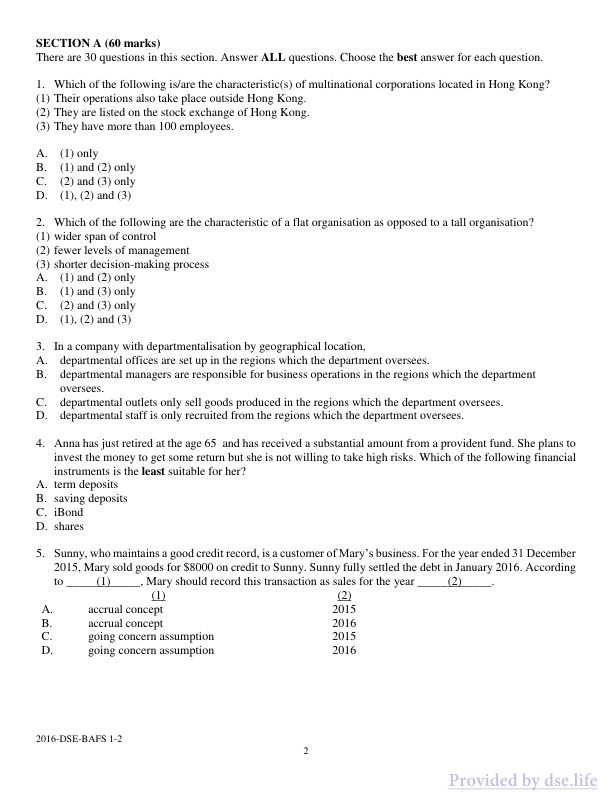

SECTION A (60 marks) There are 30 questions in this section. Answer ALL questions. Choose the best answer for each question.

-

Which of the following is/are the characteristic(s) of multinational corporations located in Hong Kong? (1) Their operations also take place outside Hong Kong. (2) They are listed on the stock exchange of Hong Kong. (3) They have more than 100 employees. A. (1) only B. (1) and (2) only C. (2) and (3) only D. (1), (2) and (3)

-

Which of the following are the characteristics of a flat organisation as opposed to a tall organisation? (1) wider span of control (2) fewer levels of management (3) shorter decision-making process A. (1) and (2) only B. (1) and (3) only C. (2) and (3) only D. (1), (2) and (3)

-

In a company with departmentalisation by geographical location, A. departmental offices are set up in the regions which the department oversees. B. departmental managers are responsible for business operations in the regions which the department oversees. C. departmental outlets only sell goods produced in the regions which the department oversees. D. departmental staff is only recruited from the regions which the department oversees.

-

Anna has just retired at the age 65 and has received a substantial amount from a provident fund. She plans to invest the money to get some return but she is not willing to take high risks. Which of the following financial instruments is the least suitable for her? A. term deposits B. saving deposits C. iBond D. shares

-

Sunny, who maintains a good credit record, is a customer of Mary’s business. For the year ended 31 December 2015, Mary sold goods for $8000 on credit to Sunny. Sunny fully settled the debt in January 2016. According to __, Mary should record this transaction as sales for the year ____. A. accrual concept 2015 B. accrual concept 2016 C. going concern assumption 2015 D. going concern assumption 2016

2016-DSE-BAFS 1-2 2 Provided by dse.life

真题 Paper 2a(中文)

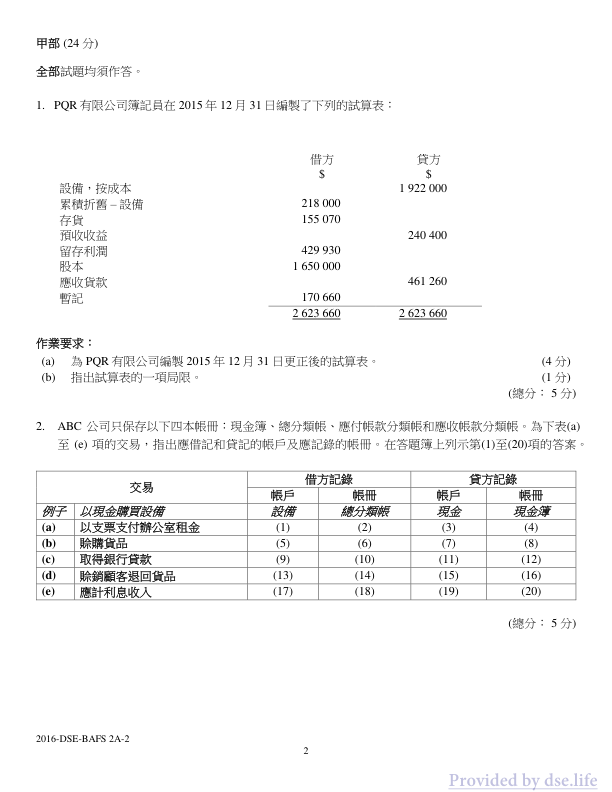

甲部(24分)

全部试题均须作答。

- PQR有限公司簿記員在2015年12月31日編製了下列的試算表:

| 設備,按成本 | $ | 1 922 000 |

|---|---|---|

| 累積折舊 - 設備 | 218 000 | |

| 存貨 | 155 070 | |

| 預收收益 | 240 400 | |

| 留存利潤 | 429 930 | |

| 股本 | 1 650 000 | |

| 應收賬款 | 461 260 | |

| 暫記 | 170 660 | |

| 2 623 660 | ||

| 2 623 660 |

作業要求: (a) 為PQR有限公司編製2015年12月31日更正後的試算表。 (4 分) (b) 指出試算表的一项局限。(1 分) (總分:5 分)

- ABC公司只保存以下四本帳冊:現金簿、總分類帳、應付帳款分類帳和應收帳款分類帳。為下表(a)至(e)項的交易,指出應借記和貸記的帳戶及應記錄的帳冊。在答题薄上列示第(1)至(20)項的答案。

| 交易 | 借方記錄帳戶 | 借方記錄帳冊 | 貸方記錄帳戶 | 貸方記錄帳冊 |

|---|---|---|---|---|

| 例子 | 以現金購買設備 | 設備 | 總分類帳 | 現金 |

| (a) 以支票支付辦公室租金 | (1) | (2) | (3) | (4) |

| (b) 除購貨品 | (5) | (6) | (7) | (8) |

| (c) 取得銀行貸款 | (9) | (10) | (11) | (12) |

| (d) 除銷顧客退回貨品 | (13) | (14) | (15) | (16) |

| (e) 應計利息收入 | (17) | (18) | (19) | (20) |

(總分:5 分)

2016-DSE-BAFS 2A-2

Provided by dse.life

真题 Paper 2b(中文)

2016-DSE 企業、會計與財務概論 卷二乙

香港考試及評核局 2016年香港中學文憑考試

企業、會計與財務概論 試卷二乙 商業管理單元

本試卷必須用中文作答 兩小時十五分鐘完卷(上午十時三十分至下午十二時四十五分)

考生须知: (一) 本試卷分為三部分。 (二) 甲、乙兩部全部試題均須作答,丙部兩道試題中選答一題。 (三) 答案須寫在答题簿上,每题(非指分题)必须另起新页作答。

2016-DSE-BAFS 2B-1 25

考试结束前不可将试卷带离考场

Provided by dse.life

真题 Paper 2a(英文)

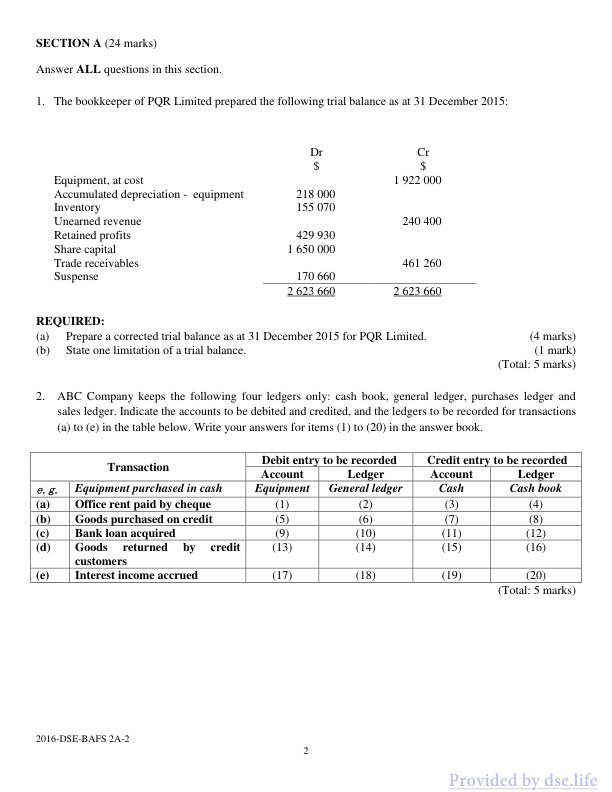

SECTION A (24 marks) Answer ALL questions in this section.

- The bookkeeper of PQR Limited prepared the following trial balance as at 31 December 2015:

| Dr $ | Cr $ | |

|---|---|---|

| Equipment, at cost | 1 922 000 | |

| Accumulated depreciation - equipment | 218 000 | |

| Inventory | 155 070 | |

| Unearned revenue | 240 400 | |

| Retained profits | 429 930 | |

| Share capital | 1 650 000 | |

| Trade receivables | 170 660 | 461 260 |

| Suspense | 2 623 660 | 2 623 660 |

REQUIRED: (a) Prepare a corrected trial balance as at 31 December 2015 for PQR Limited. (4 marks)

(b) State one limitation of a trial balance. (1 mark) (Total: 5 marks)

- ABC Company keeps the following four ledgers only: cash book, general ledger, purchases ledger and sales ledger. Indicate the accounts to be debited and credited, and the ledgers to be recorded for transactions (a) to (e) in the table below. Write your answers for items (1) to (20) in the answer book.

| Transaction | Debit entry to be recorded | Credit entry to be recorded |

|---|---|---|

| e.g. Equipment purchased in cash | Account | Ledger |

| (a) Office rent paid by cheque | (1) | (2) |

| (b) Goods purchased on credit | (5) | (6) |

| (c) Bank loan acquired | (9) | (10) |

| (d) Goods returned by credit customers | (13) | (14) |

| (e) Interest income accrued | (17) | (18) |

(Total: 5 marks)

2016-DSE-BAFS 2A-2 2

Provided by dse.life

真题 Paper 2b(英文)

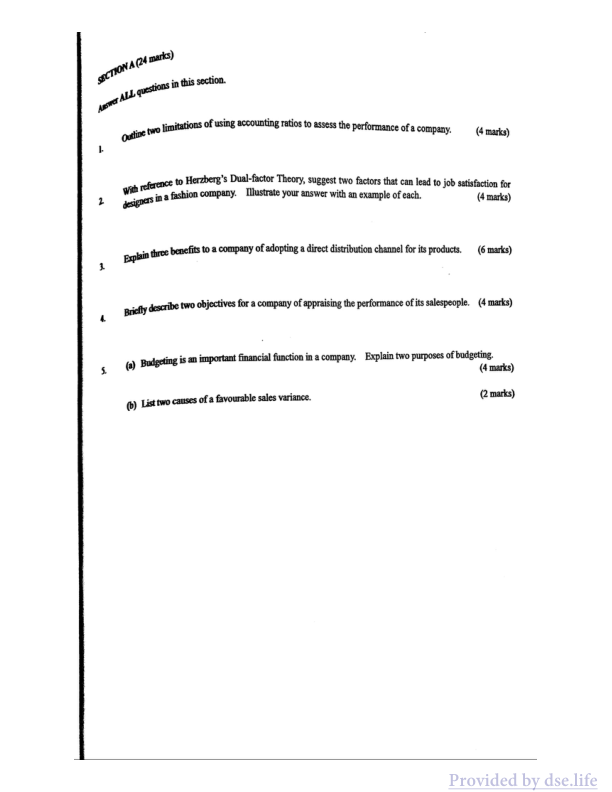

SECTION A (24 marks) Answer ALL questions in this section.

-

Outline two limitations of using accounting ratios to assess the performance of a company. (4 marks)

-

With reference to Herzberg's Dual-factor Theory, suggest two factors that can lead to job satisfaction for designers in a fashion company. Illustrate your answer with an example of each. (4 marks)

-

Explain three benefits to a company of adopting a direct distribution channel for its products. (6 marks)

-

Briefly describe two objectives for a company of appraising the performance of its salespeople. (4 marks)

-

(a) Budgeting is an important financial function in a company. Explain two purposes of budgeting. (4 marks)

(b) List two causes of a favourable sales variance. (2 marks)

Provided by dse.life